HiPOS Weekly Update: Staying Between the Lines Expiration Edition

By Derek Moore

This Friday marks expiration day for what turned out to be a short iron condor position in our primary HiPOS Conservative strategy. As a reminder, a short call spread was initially established. Then, when the markets gapped down, and volatility jumped higher, ZEGA’s traders also found a short put spread that qualified and was added to the position.

This type of position can be a little different to follow as you really would like the market to stay between the lines representing the short call strike and short put strike. As we can see above in the graph, thus far it has done just that. Also, the trade nicely has stayed above/below the purple curved defensive posture lines.

It is also worth noting that when we established each of the positions, the time to expiration was much shorter than typical due to the overhang of higher volatility. Simply stated, this means we can get more premium over a shorter amount of time, while still qualifying under our strict rules.

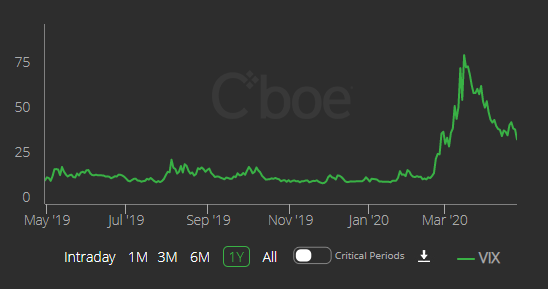

Source: CBOE

While the VIX Index is off its highest levels, it remains above 30 and has not seen a close below that since February 26th of this year. HiPOS is a strategy that can take advantage of higher volatility. Especially in orderly trading environments where the realized volatility is below the volatility priced into spread premiums.

So, what happens this week? Unless there are extreme movements in the underlying S&P 500 Index, we would most likely not see much change in account values as most of the time premium has already been experienced in the positions.

Should volatility remain elevated, ZEGA’s traders most likely will be able to have a short turn around time before finding the next HiPOS position.