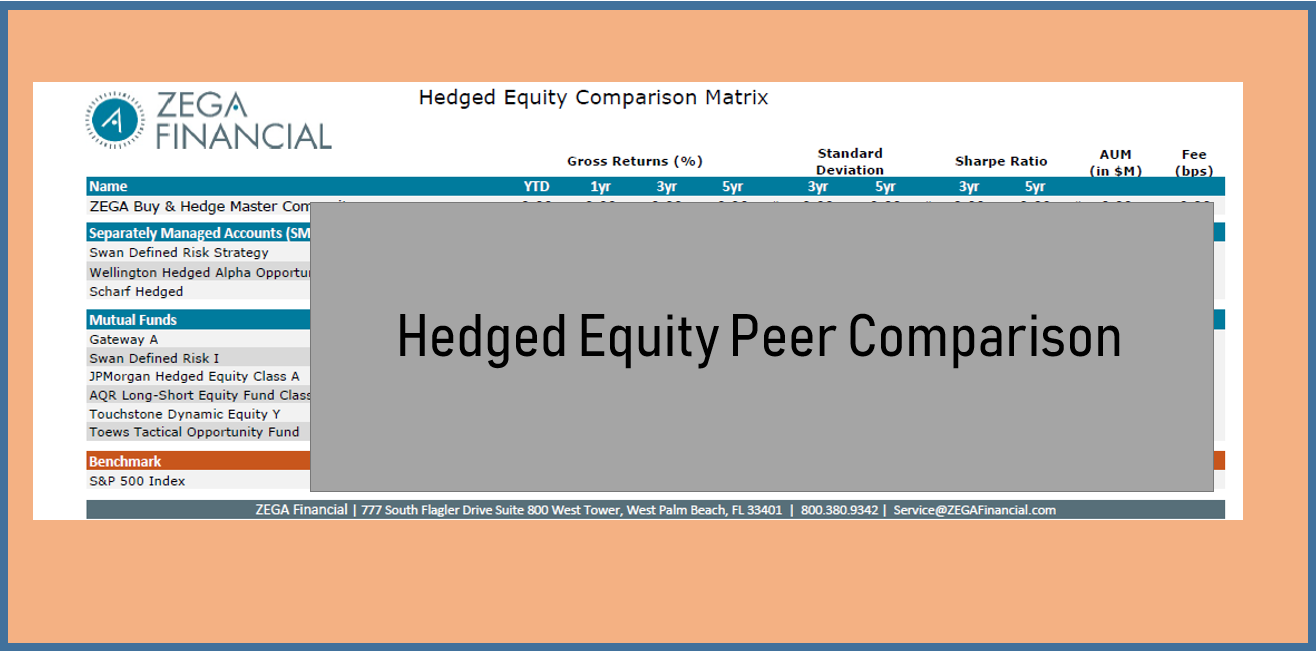

Hedged Equity Peer Comparison Performance

By Derek Moore

With the close of 2018 performance release, we can reflect on the year past and the future. As you all know the S&P 500 Index had its first down year since 2008 closing down -4.38%.

As we review our peer comparison list, we can see a bit of variance between the combination of separately managed accounts and mutual funds in the space. Only 3 other strategies aside from ZEGA’s outperformed the S&P 500 Index. Over the 3-year period ZEGA returned the highest percent gain while also delivering the highest Sharpe Ratio.

What is Sharpe Ratio?

Sharpe Ratio as a reminder, is a way to marry the relationship between return and volatility in returns via the standard deviation. It simply takes the return minus a risk-free rate (3 month or 1-year treasury) and divided by the standard deviation. The higher the number the better. Put another way, how bumpy was the ride to a return?

2018 saw the equity markets reach new all-time highs during September only to suffer one of the worst quarters in history during Q4. We also say bond market values plummet as fear came into the market and liquidity in the short run affected prices as investors pulled money out of bond funds.

We utilize short duration bond funds that typically hold until maturity. As such, outside of defaults, would expect bonds that selloff to eventually pullback closer and closer to their final par value. While the 2018 full year performance includes unrealized market, value drops in those bonds, thus far in 2019 we have seen a material recovery in bond prices.

This along with the recovery in overall markets should produce a positive start to Q1 2019.