Buy and Hedge Retirement Fixed Income Update

Recently some advisors have reached out for an update around the income portion of ZEGA’s Buy and Hedge Retirement Strategy. As many of you know this strategy looks to capture around 75% of the S&P 500 Index upside while putting a floor in the equity downside around -8%. We do this by using options as stock replacement and essentially only spend 7%-9% to make portfolios feel as if they are 100% invested in the market. The remaining 91%-93% of the portfolio is invested into a risk managed income strategy, we refer to as the “Income Portion” of the strategy. Currently, and for the last two years, we have used short duration bonds. Until recently that comprised almost entirely of short duration hold to maturity high yield.

The return target of the Income Portion for Buy and Hedge Retirement is somewhere between 3.5-4%. That is enough to lower our cost of hedging to an acceptable level each year. The Income Portion is not meant to diversify risk, but simply generate returns that help reduce the cost of hedging.

Historically, fixed income, even short duration high yield, has shown much less volatility on a year to year basis that stocks.

As we can see above using the Barclay’s High Yield 1-3 YR Total Return Index, the standard deviation is much less relative to the S&P 500.

What Is Going on With the Short Duration High Yield Portion?

HY Bulletshares ETF Total Return

Above are listed in the table the various Bulletshare ETFs we have been or are currently deploying in accounts and the total returns including dividends over recent periods. The reason we favor this vehicle is that they have the hold to maturity characteristic. This feature reduces the impact of interest rate risk as the position within the fund are held to maturity or callable date. That means we expect the bonds to close out close to or at par value.

As we can see while the total returns are still positive year to date, they are less than the expected return we targeted of 3.5% for 2018. Provided we do not see outsized defaults in the high yield market, the guidance given to us is that market values should tack back towards par value as maturity nears.

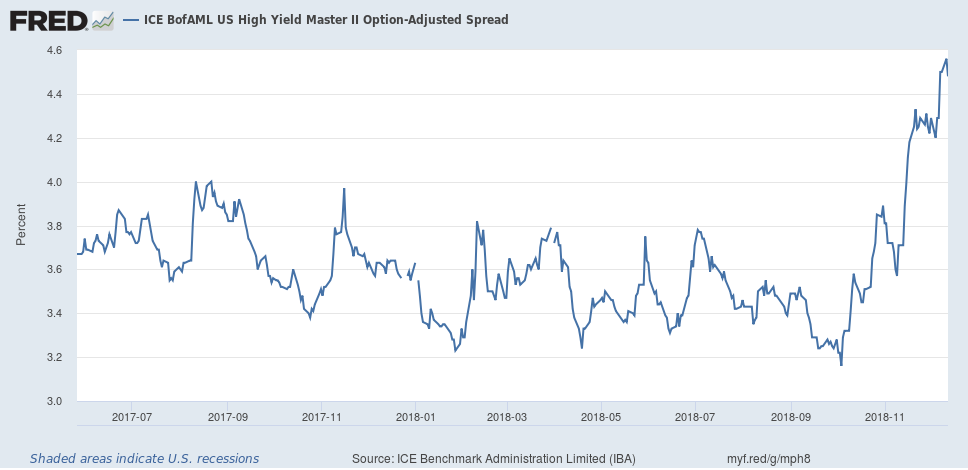

So Why the Change Lower in Market Values?

While we’re happy to discuss the details of what is going on in the HY market it’s a probably a little too detailed for a blog post. But suffice it to say, underlying values of the Bullet Share ETFs has dropped causing the underperformance. This reflects the widening of spreads between Treasuries and High Yield.

Spreads can widen if Treasuries rates fall, or if high yield sells off thus increasing yields. Below we can see how this spread has widened of late.

Source: Federal Reserve Bank of St. Louis

In our discussion with the team over at Invesco they pointed to a couple things around the Bulletshare Short Duration ETF. First, they have shown to hold up better compared with say the HYG ETF which is considered a benchmark for the High Yield asset class. They also pointed to a few things regarding the strong health of the underlying companies whose debt is contained in the Bulletshares.

• HY leverage continued to tick down in Q3.Debt/EBITDA hit 3.86X at the end of Q3 which is a post crisis low

• HY revenue growth remains robust with growth of 8.7%, 10.8%, 11.3% in Q1, Q2, and Q3 2018 respectively

Source: Invesco

The above reflects their view of continued strength in the fundamentals of the high yield market

Do Recent Rises in US Treasury Yields Provide Opportunity for Fixed Income Allocations in Buy and Hedge Retirement?

The quick answer is yes. ZEGA is always reviewing our strategies to see if there are ways to increase benefits to advisors and their clients. Post 2008 as most of you know, the Federal Reserve kept interest rates near zero which mean that yields in Treasuries were just non-existent. This changed when the Fed began rising rates for the first time in a decade as we can see in the graph below.

Source: Federal Reserve Bank of St. Louis

We may look to substitute shorter duration US Treasuries, which have less risk, for portions of our fixed income allocation. Simply put, treasuries haven’t been an option for a decade but with yields beginning to normalize, they now are part of the discussion. You will begin to see a migration to Treasuries as a portion of our income mix as long as short-term yields are above 2.5%

Summary

To summarize

- The fixed income space has had a year just as tough as equities as yield spreads have widened.

- While we don’t use fixed income to diversify risk exposure, we do use it as a means of funding our cost of hedging for Buy and Hedge Retirement.

- As treasury rates move higher, they become a more attractive option to help reach the target of 3.5-4% for the income portion of the portfolio.

- Be on the lookout for a partial migration from High Yield into 2-year treasuries in the Buy and Hedge Retirement portfolio.

As we move towards 2019, its important to remember why you are placing Buy and Hedge Retirement in portfolios.

- You want to avoid materially downside equity moves

- You want to reduce portfolio volatility offering superior risk adjusted returns

- Your clients still need growth but cannot afford to have 100% equity type risk

- And your clients want to be able to sleep a little better at night knowing they have downside protection

As always, the ZEGA team is happy to help with any questions around this or other strategies we run.